Defining Structured Settlements

A structured settlement is a financial arrangement that provides a claimant with a series of payments over time, rather than a single lump sum. This approach is often used in personal injury cases, particularly those involving catastrophic injuries that require ongoing medical care and support. The core idea is to create a reliable financial foundation that lasts for the duration of the claimant’s needs. Instead of managing a large amount of money all at once, which can be challenging, the claimant receives regular, predictable payments. These payments are typically funded by an annuity purchased by the defendant or their insurer, which guarantees the future payments to the claimant. This method aims to provide financial security and stability, especially when dealing with long-term care requirements that can span many years or even a lifetime.

The Role in Addressing Catastrophic Injuries

When someone experiences a catastrophic injury, the financial implications can be immense and long-lasting. These injuries often require extensive medical treatment, rehabilitation, specialized equipment, and ongoing personal care. A structured settlement plays a vital role in addressing these complex needs by providing a consistent and dependable source of funds. Unlike a lump sum, which can be quickly depleted through mismanagement or unexpected expenses, a structured settlement ensures that money is available when it’s needed most, for as long as it’s needed. This predictability is especially important for individuals who face lifelong care requirements. It allows them and their families to focus on recovery and quality of life without the constant worry of running out of money for essential medical services and support.

Benefits Over Lump Sum Payouts

Choosing a structured settlement over a lump sum payout offers several distinct advantages, particularly for long-term care needs:

- Guaranteed Income: Payments are typically guaranteed by a highly rated life insurance company, providing a secure and predictable income stream. This removes the risk associated with investing a lump sum and hoping for consistent returns.

- Tax Advantages: In most cases, the periodic payments received from a structured settlement are entirely tax-free. This means the full amount of each payment goes towards care and living expenses, without deductions for federal or state income taxes.

- Protection Against Mismanagement: The structured nature of the payments prevents the claimant from spending the entire settlement amount prematurely. This is a significant benefit for individuals who may not have experience managing large sums of money or who are vulnerable to financial exploitation.

- Inflation Protection: Payments can be structured to increase over time, often tied to an inflation index. This ensures that the purchasing power of the settlement keeps pace with the rising cost of living and medical care, maintaining the adequacy of the funds over the long term.

Securing Financial Stability Through Structured Payments

Guaranteed, Tax-Free Income Streams

One of the most significant advantages of a structured settlement is the creation of a reliable, tax-free income stream. Unlike a lump sum that can be quickly spent or lost, structured payments are distributed over time according to a predetermined schedule. This means recipients receive funds consistently, which is particularly important for managing ongoing long-term care expenses. These payments are generally free from federal income tax under IRS Code Section 104(a)(2), allowing recipients to keep the full amount awarded without worrying about tax liabilities. This predictable cash flow helps individuals manage their budgets more effectively and focus on their health rather than financial management. It provides a sense of security, knowing that funds will be available when needed for medical treatments, living expenses, or other care-related costs. This steady financial foundation is a key component of long-term planning, offering peace of mind for individuals and their families. For more on how these arrangements work, you can look into structured settlement benefits.

Protection Against Market Volatility

Structured settlements offer a significant advantage by being insulated from the unpredictable nature of financial markets. When a settlement is paid as a lump sum, individuals might choose to invest it. However, investments can lose value due to market downturns, potentially jeopardizing the funds needed for long-term care. Structured settlements, on the other hand, are typically backed by highly rated life insurance companies. This means the payments are guaranteed by the insurer, not subject to stock market fluctuations. This stability provides a secure financial buffer, ensuring that the settlement amount remains intact and accessible regardless of economic conditions. This protection is vital for individuals who rely on their settlement for lifelong care needs, as it removes the risk of investment losses impacting their financial future. This insulation from market forces is a core feature that distinguishes structured settlements from other financial planning tools, providing financial stability.

Alleviating Financial Anxiety

Dealing with a serious injury or illness and the associated long-term care needs can be incredibly stressful. The financial burden often adds to this anxiety. Structured settlements help alleviate this by providing a clear and predictable financial path forward. Knowing that regular, tax-free payments will arrive on a set schedule reduces the constant worry about how to pay for upcoming medical bills or daily living expenses. This predictability allows individuals to concentrate their energy on recovery and quality of life, rather than on the day-to-day management of finances or the fear of running out of money. The structured nature of the payments acts as a financial safety net, offering peace of mind and reducing the emotional toll associated with long-term care planning. This can lead to improved well-being for both the injured party and their family members.

Customizing Payment Schedules for Evolving Needs

Structured settlements offer a remarkable degree of flexibility, allowing for payment plans that can be precisely shaped to fit an individual’s unique circumstances and how those circumstances might change over time. This isn’t a one-size-fits-all approach; rather, it’s about building a financial roadmap that aligns with future requirements.

Tailoring Payments to Specific Requirements

The initial setup of a structured settlement involves careful consideration of immediate and near-term needs. For instance, following a significant injury, there might be substantial upfront costs for specialized equipment, home modifications, or immediate medical treatments. The payment schedule can be designed to provide larger sums at these critical junctures. Conversely, if the primary concern is long-term care, the schedule might be weighted towards later years when those costs are projected to increase. This careful calibration means funds are available precisely when they are most needed, preventing premature depletion and ensuring that essential expenses are met.

Incorporating Escalating Payments for Inflation

One of the significant advantages of structured settlements is their ability to combat the erosive effects of inflation. The cost of goods and services, particularly medical care, tends to rise over time. To address this, payment schedules can include escalating payments, often referred to as step annuities. These are designed to increase at predetermined intervals or by a set percentage each year. This built-in growth helps maintain the purchasing power of the settlement funds, ensuring that the amount received in the future can still cover the same level of care or expenses as it could when the settlement was first established. This foresight is vital for long-term financial security.

Deferred Lump Sums and Milestone Payments

Beyond regular income streams, structured settlements can also accommodate significant future financial needs through deferred lump sums. These are larger, one-time payments scheduled for specific future dates. This feature can be incredibly useful for planned expenses such as:

- Future educational costs for dependents.

- Major home renovations or upgrades.

- Replacement of durable medical equipment.

- Significant medical procedures planned years in advance.

These milestone payments provide a substantial financial cushion precisely when a large expense is anticipated, adding another layer of practical financial planning to the settlement structure.

Preserving Eligibility for Public Assistance

For individuals who rely on government programs for ongoing support, receiving a settlement can present a complex situation. A large, one-time payment, often called a lump sum, can quickly make someone ineligible for benefits like Medicaid or Supplemental Security Income (SSI). This is because these programs have strict limits on the amount of assets an individual can own. When a settlement is paid out as a lump sum, it counts towards that asset limit, potentially cutting off vital assistance.

Impact of Lump Sums on Benefit Eligibility

When a settlement is received as a single, large payment, it’s generally considered an asset. Government agencies that administer programs like Medicaid and SSI look at your total financial resources. If this lump sum pushes your assets over the allowed threshold, your eligibility for these benefits can be suspended or terminated. This can be a significant problem, especially if the settlement funds are intended to cover long-term care needs that public assistance would otherwise help pay for. It creates a difficult choice: use the settlement money and lose public benefits, or try to manage without the settlement funds to keep benefits active.

Utilizing Special Needs Trusts

One common strategy to avoid this issue is to use a Special Needs Trust (SNT). This is a legal arrangement designed specifically for individuals with disabilities or chronic illnesses. When settlement funds are placed into an SNT, they are managed by a trustee but are not counted as the beneficiary’s personal assets for the purpose of public benefit eligibility. This allows the funds to be used for specific needs that public assistance might not cover, such as:

- Specialized medical equipment not covered by insurance or Medicaid.

- Therapeutic services or programs.

- Home modifications to improve accessibility.

- Educational or vocational training.

- Assistance with daily living expenses beyond what SSI provides.

An SNT provides a way to supplement public benefits without jeopardizing them, offering a more secure financial future.

Coordination with Medicaid and SSI

Careful planning is key when setting up a structured settlement to ensure it works alongside existing public assistance. This often involves working with legal professionals who understand both settlement structures and public benefit rules. They can help design the payment schedule and trust arrangements to meet specific needs while staying within program guidelines. For instance, payments can sometimes be structured to be small enough not to affect eligibility, or they can be directed into an SNT. The goal is to create a financial plan that provides for long-term care without creating a gap in essential government support. Consulting with an elder law attorney or a benefits specialist early in the process is highly recommended to explore all options and make informed decisions.

Addressing Concerns and Ensuring Flexibility

Adapting to Changing Medical Needs

Life has a way of throwing curveballs, and for individuals relying on structured settlements for long-term care, this often means adapting to evolving medical needs. A primary concern is whether a settlement can accommodate unexpected health changes or the need for more advanced care down the line. While structured settlements are built on predictability, they aren’t entirely rigid. It’s possible to build some flexibility into the initial agreement. This might involve setting aside funds for potential future medical equipment or including provisions for periodic reviews to adjust payments if circumstances significantly change. However, it’s important to understand that modifying an established payment schedule after the settlement is finalized can be a complex process, often requiring court approval. This is why careful planning during the initial structuring phase is so important to anticipate as many future needs as possible.

Understanding Annuity Ownership

When you receive a structured settlement, you’re typically not the direct owner of the annuity that funds it. Instead, a third party, often a life insurance company, owns the annuity and makes payments to you according to the settlement agreement. This arrangement provides a layer of security, as the payments are backed by the financial strength of the insurer. However, it also means you don’t have direct control over the annuity itself. You can’t, for example, cash it out or change its terms unilaterally. Understanding this distinction is key to knowing your rights and limitations within the settlement.

The Option to Sell Future Payments

Life circumstances can change, and sometimes an immediate need for a lump sum arises. For those with structured settlements, there is an option to sell some or all of their future payments to a third-party company. This process, often called factoring, provides quick access to cash. However, it’s crucial to be aware that these companies typically purchase future payments at a significant discount. This means you will receive substantially less than the total amount you would have received over time. Before considering such a sale, it is highly recommended to:

- Thoroughly review the terms of your original settlement agreement.

- Consult with a qualified financial advisor to assess the long-term impact on your financial stability.

- Seek legal counsel to understand the process and ensure your rights are protected.

This option should generally be viewed as a last resort, as it can compromise the long-term financial security the structured settlement was designed to provide.

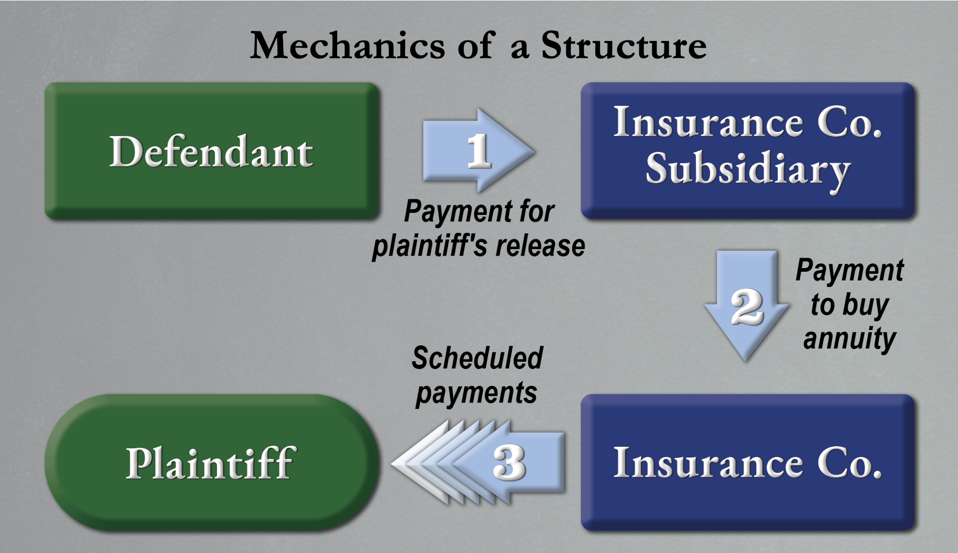

The Mechanics of Establishing a Structured Settlement

Setting up a structured settlement involves a few key steps to make sure everything is put in place correctly. It’s not just a simple handshake deal; there’s a process to follow.

Negotiation and Agreement Between Parties

This is where the whole thing really gets started. Usually, the person who was injured and their legal team will talk with the other side, often an insurance company or the party responsible for the injury. They discuss whether a structured settlement makes sense for the situation. Both sides have to agree on the terms. This means figuring out how much money will be paid, when it will be paid, and for how long. The goal is to create a payment plan that truly fits the injured person’s future needs, like covering medical bills or living expenses.

The Role of Court Approval

Sometimes, a judge needs to sign off on the deal. This is especially true if the person receiving the money is a minor, or if they can’t manage their own finances. The court’s job is to make sure the agreement is fair and that it’s really in the best interest of the person who was hurt. It’s an extra layer of protection to confirm the long-term financial plan is solid.

Expert Collaboration in Payment Schedule Design

Creating the actual payment schedule isn’t usually done by just one person. It often involves a team of professionals. Think of life care planners, medical experts, and financial advisors. They all work together with the lawyers. These experts bring specific knowledge to help figure out:

- What future medical costs might look like.

- How inflation could affect the cost of living over time.

- When specific large expenses might come up, like needing new equipment or home modifications.

Their input helps build a payment plan that’s realistic and covers all the bases for the long haul.

Background Reading

- JJSjustice.com

- Nursing Home Center

- Lawfirm.com

- Millerandzois.com

- Seniorjustice.com

- Levin and Perconti Law